Fundraising Event Regulations Nonprofits Have to Follow

Fundraising events are the heart of every non-profit organization. They are a fun way for these organizations to raise money for a good cause and attract public attention. In fact, most wouldn’t exist or be sustainable without holding regular fundraising events.

Hosting a fundraising event requires a lot of financial resources and hard work from an organization. And the government has made it more challenging by requiring permits and enforcing specific state and federal regulations on how non-profits should host these events.

To help you stay compliant, we discuss some important non-profit fundraising laws that every charitable organization in the United States should be familiar with when fundraising.

1. Regulations for 501 (c)(3) Organizations

501(c)(3) is a section of the United States Internal Revenue Code that grants non-profit organizations federal tax exemptions. 501(c)(3) organizations are commonly referred to as charitable organizations and fall into three primary categories: public charities, private operating foundations, and private foundations.

501(c)(3) Requirements

To qualify as a 501(c)(3) organization, a non-profit organization must exist for one or more of these exempt purposes

-

Charitable

-

Scientific

-

Religious

-

Educational

-

Literary

-

Testing for public safety

-

Child and animal cruelty prevention

-

Fostering amateur sports competitions

Beyond serving these exempt purposes, a non-profit must also meet several other requirements to qualify:

-

None of its earnings may profit any private individual

-

It may not attempt to influence legislation as a significant part of its activities

-

It may not participate in any campaign activity against or for political candidates

Tax Benefits of Being a 501(c)(3) Organization

One of the most significant benefits of earning a 501(c)(3) status is that it allows donors to reduce their donations for federal and state income tax purposes.

The status benefits non-profits directly by:

-

Allowing them to receive grants from the government and private foundations

-

Exempting them from many local, state, and federal taxes

-

Giving them special bulk postage discounts and non-profit advertising rates

-

Exempting them from lawsuits

Unrelated Business Income

Some activities are unrelated to a non-profit’s tax-exempt purposes.

Under such circumstances, funds generated from these activities may be categorized as Unrelated Business Income (UBI). Accordingly, the law requires all registered charitable organizations to pay taxes on any UBI. Under the Internal Revenue Service rules, this is referred to as Unrelated Business Income Taxation (UBIT).

To reduce confusion on what qualifies as UBI, the IRS has established a three-part test for it. Under these three circumstances, income could be taxable under UBI:

-

Income is from a business or trade

-

The income-producing activity is something that results from a continuously operated business

-

The business of trade doesn’t substantially relate to the organization’s exempt purpose

Tax laws offer some exceptions for what is considered UBI:

-

When volunteers carry out all the activities

-

When activities are primarily carried out for the convenience of the non-profit’s members

-

When the profits from the business are all donated back to the organization

A non-profit that has banked $1,000 or more of gross income from unrelated businesses must file a Form 990-T. It must also pay estimated tax if it expects its UBIT to exceed $500 for the year.

2. Regulations for fundraising events (games)

Fundraising events are state-regulated.

It’s, therefore, crucial to look up whether your state allows charitable non-profits to hold these games and activities. If it does, your organization will need to apply for a state license. In addition, it’s essential to know that certain types of events, including raffles, gambling, auctions, and events that serve alcoholic beverages, come with strict regulations attached.

These regulations may vary from state to state.

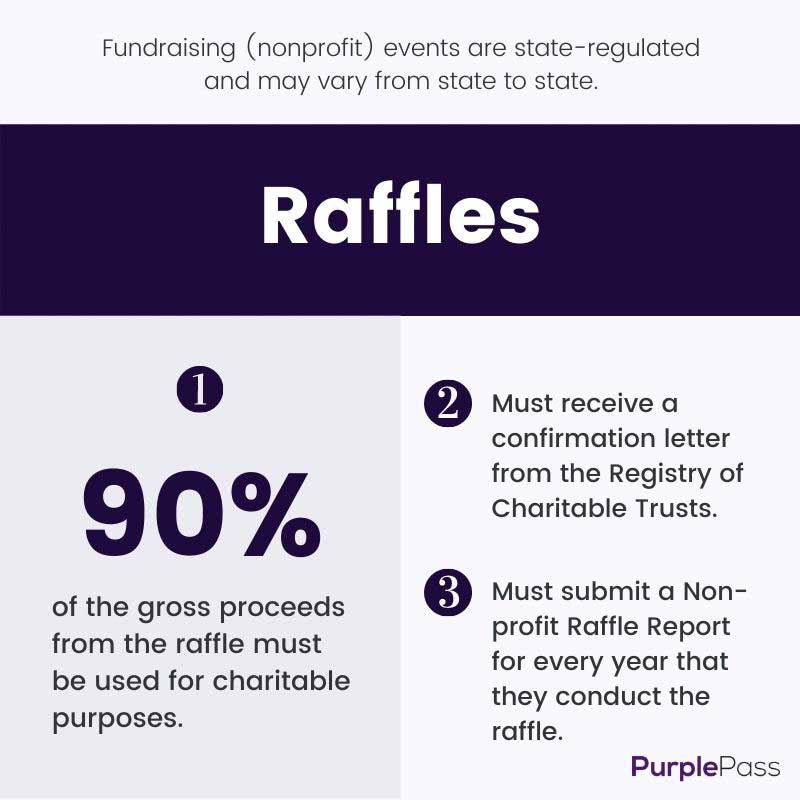

Raffles

We consider any event in which participants buy a ticket for a chance to win a prize a raffle. Non-profit organizations may host a raffle if they meet the following criteria:

-

At least 90% of the gross proceeds from the raffle must be used for charitable purposes.

-

The organization must register with the Attorney General’s Registry for Charitable Trusts before conducting the raffle and submit an application fee. No raffle activities should take place before receiving a confirmation letter from the Registry of Charitable Trusts.

-

The organization must submit a Non-profit Raffle Report for every year that they conduct the raffle.

Auctions

An auction is defined as an activity where bidders compete against each other for an item. A sales tax must be paid on the items auctioned, and a selling permit may be required.

Sales tax

-

It’s only applicable to tangible property

-

This tax applies to the gross receipts from the sale, even if it falls below or exceeds the item’s actual value

-

Sales tax is the responsibility of the organization, either by paying themselves or requiring the donor to pay it to the organization

-

The organization must report both un-taxable and taxable sales on the return, whether it owes taxes or has no sales

Seller’s Permits

A seller’s permit is required if the organization intends to lease or sell any tangible property (over three items in 12 months) that would typically be subject to sales tax.

Tax deductibles

Not all payments in an auction are considered tax-deductible.

The amount that can be tax-deductible is that which the donor has paid above the market value of the item purchased. Additionally, when a donor contributes an item to the auction, the value of the contribution is determined by the market value, not an arbitrary amount determined by the donor or the organization.

Gaming

Gaming events may include casino nights, bingo, poker nights, or any other activity involving gambling.

To host an event, an organization needs to meet the following requirements:

-

Submit an Annual Registration Form to the Bureau of Gambling Control for approval before the event

-

The organization must mail no less than 30 days or not more than 90 days to the event date

-

Pay a non-refundable registration fee

There are also limitations on the prizes that participants can win and the games that they can play:

-

Only controlled games that appear on the BGC Standard Game List may be played at these events

-

Hold a gambling fundraiser at most once per calendar year

-

Not hold the games online

-

All participants must not be under 21 years

-

Refrain from giving out cash prizes and give out prizes donated to the fundraiser

-

Each prize shouldn’t exceed $500, and the total cash value of all prizes shouldn't exceed $5,000

-

Non-profit organizations are also required to file a W-2G to the IRS and withhold tax from the winnings.

Serving Alcoholic Beverages

To serve alcohol at a fundraising event, you must obtain a permit from your relevant liquor licensing authority.

As an organization intending to serve alcohol at an event, you must keep in mind that:

-

The event should be limited to guests 21 and over

-

You are liable to damage caused by guests who consume too much

-

Alcoholic beverages are taxable unless included in the price of a meal

3. Regulations on donation receipts

Donation receipts are written records that show that a party made a gift to a registered 501(c)(3) non-profit. If the donor contribution exceeds $250, the receiving organization must acknowledge the party by a letter.

Though these non-profit laws can be confusing, non-profit organizations must understand these requirements to avoid unexpected fees, hefty penalties, and circumstances that could threaten the success of their event.